Who’s who in online card payments?

Getting paid online by a customer’s credit/debit card is as simple as getting paid by a bank transfer, and even faster. What – and, more importantly, who – is involved?

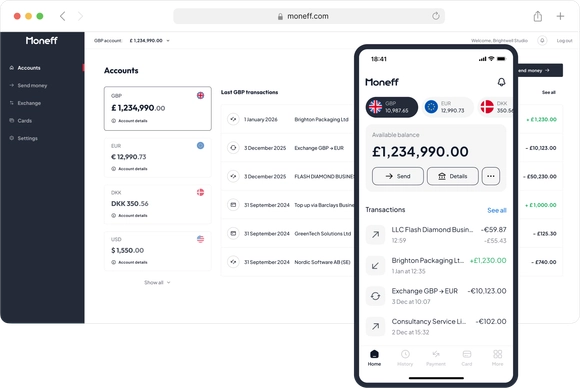

As a Safenetpay client, you have a UK account with a UK sort code and IBAN (GBP) and a European Union (EU) IBAN. If you receive a bank transfer from a customer from within the UK or the EU, the money should be available to you on the following business day. If the customer is outside the UK and the EU, the money should be available in two-to-three business days. The money will likely have to pass from the customer’s bank, and through correspondent banks in the customer’s country and the UK, before arriving in your Safenetpay account.

So, what happens if the customer wants to pay you online by way of a card transaction (CT)?

In the first instance, the CT is checked by our Anti-Fraud Management System. The aim is to reduce the risks by assessing criteria such as the geographical location of the card, the IP address and the device being used in the CT.

Then, the CT is passed through Safenetpay’s payments gateway to your acquiring bank (or acquirer). The acquirer is the bank which handles your relationships with the major card payment networks such as Visa, Mastercard or JCB. A payment gateway is an e-commerce system that helps support modern retail or other types of sales of products and services over the Internet or at brick-and-mortar stores.

In traditional retailing, with ‘bricks & mortar’ shops, the acquirer is the bank that provides you with the electronic card terminal that is used by the customer at the point of sale.

The acquirer plays a key role in entire the process, which should take seconds. It is the acquirer which decides whether to approve or reject the CT on the basis of the information it receives from the card payment network and the issuing bank.

The issuing bank is the institution which provided the card to the customer. Sometimes the card will be co-branded by the issuing bank and another organisation to which the customer has links. The issuing bank is the institution which provides the line of credit to the customer that underpins spending on a credit card. In the case of a debit card, the spending is underpinned by the customer’s deposit with the issuing bank.

If the payment to you is in a different currency to the currency of the card, the issuing bank will undertake the foreign exchange conversion that is required. The costs will be borne by the customer.

In handling the CT, the acquirer will deal directly with the card payment network, while the card payment network will deal directly with the issuing bank.

If the CT is approved by the issuing bank, that bank will confirm the fact with the card payment network. Funds will then be released by the issuing bank through the card payment network to the acquirer. The acquirer will then pay the funds to your account with Safenetpay.

Those funds can then be used by you to pay your suppliers, or transferred to another account that you hold. Of course, all requests to transfer funds out of your Safenetpay account are screened by our Anti-Fraud Management System.